Higher education

fromFortune

1 day agoIs a college degree is still worth it? Here are 3 things it can teach you that AI can't do | Fortune

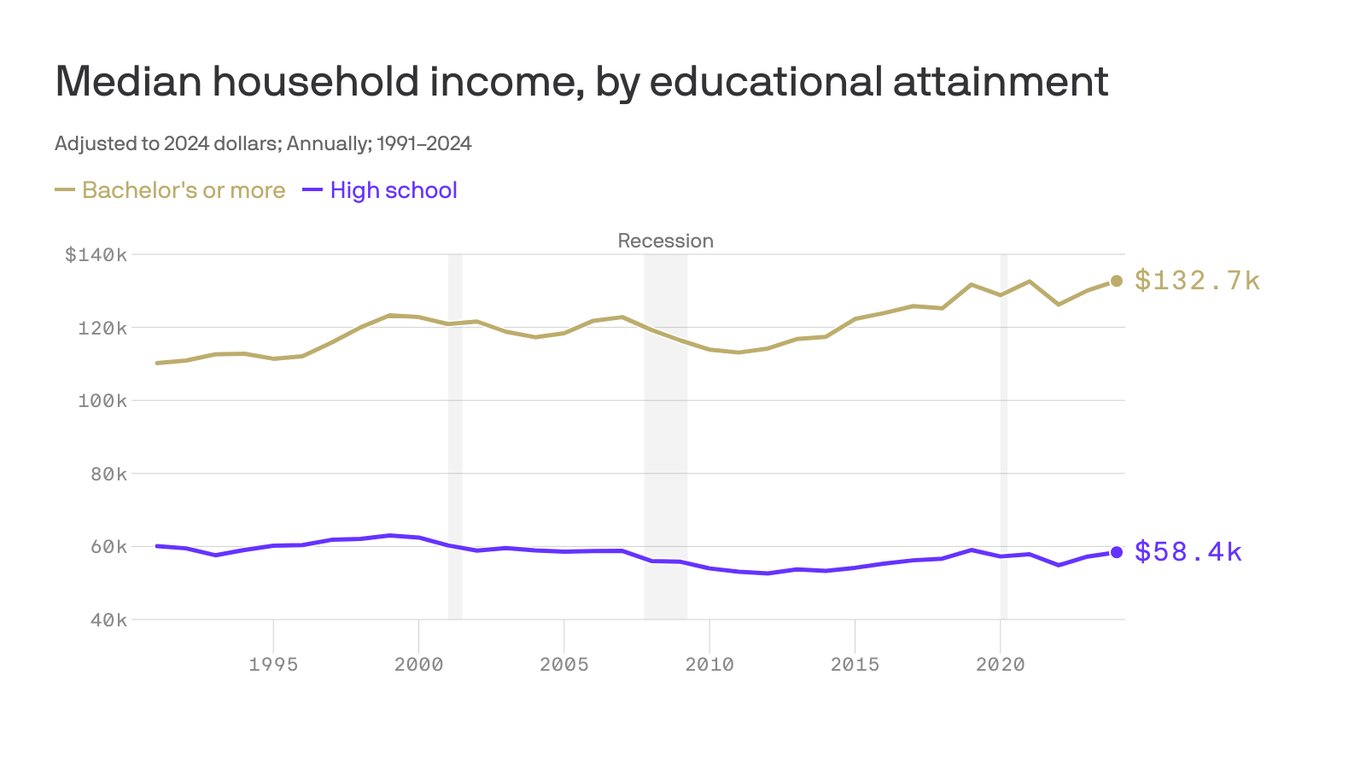

College degrees can still provide human-competitive skills like social interaction, creativity, and navigating complex environments despite AI-driven doubts about degree value.