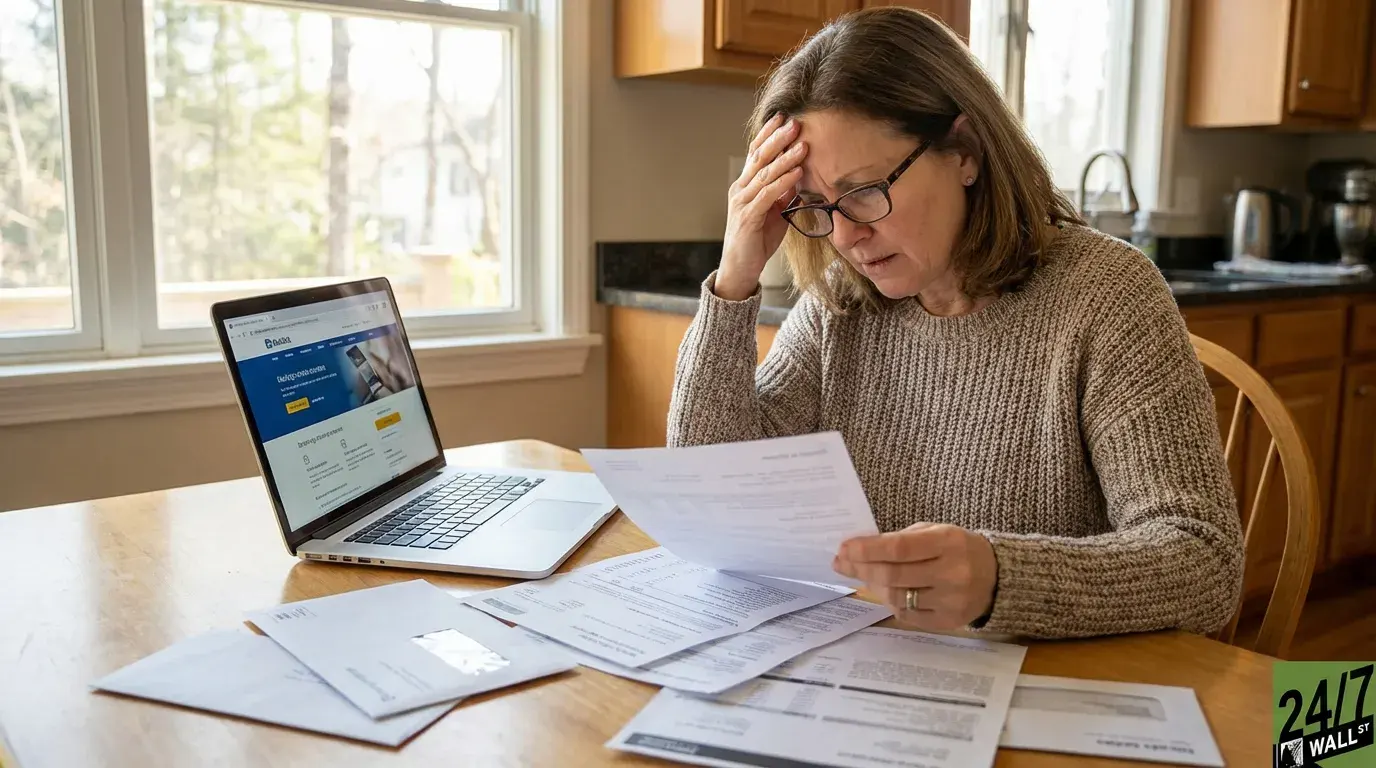

"Americans collectively owe $1.233 trillion in credit card debt, with nearly half of all cardholders carrying balances month to month at an average APR of 22.83%. Despite recent Federal Reserve rate cuts, borrowers face a persistent financial squeeze because credit card issuers maintain their markup regardless of policy changes, meaning lower Fed rates don't translate to meaningful relief for consumers paying double-digit interest on revolving debt."

"issuers add a consistent 15 to 18 percentage point markup over the prime rate, which itself sits about 3 percentage points above the Fed's rate. This cascading markup structure means that even as the Fed lowers rates, the absolute cost of credit card borrowing stays elevated-the entire rate structure simply shifts downward while maintaining the same expensive gap between what the Fed charges banks and what consumers pay on their cards."

Americans collectively owe $1.233 trillion in credit card debt, with nearly half of cardholders carrying month-to-month balances at an average APR of 22.83%. The Federal Reserve cut its benchmark rate to 3.72% in December, but credit card borrowers have seen minimal benefit because issuers add a consistent 15 to 18 percentage point markup above the prime rate, which sits roughly 3 percentage points above the Fed. Most cards charge variable APRs tied to prime while issuers keep a constant margin. Daily compounding and low minimum payments accelerate interest accumulation and trap borrowers in growing debt.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]