#micron-technology

#micron-technology

[ follow ]

#stock-market #semiconductors #ai-infrastructure #ai-memory #memory-chips #high-bandwidth-memory #dram #sandisk #ai

from24/7 Wall St.

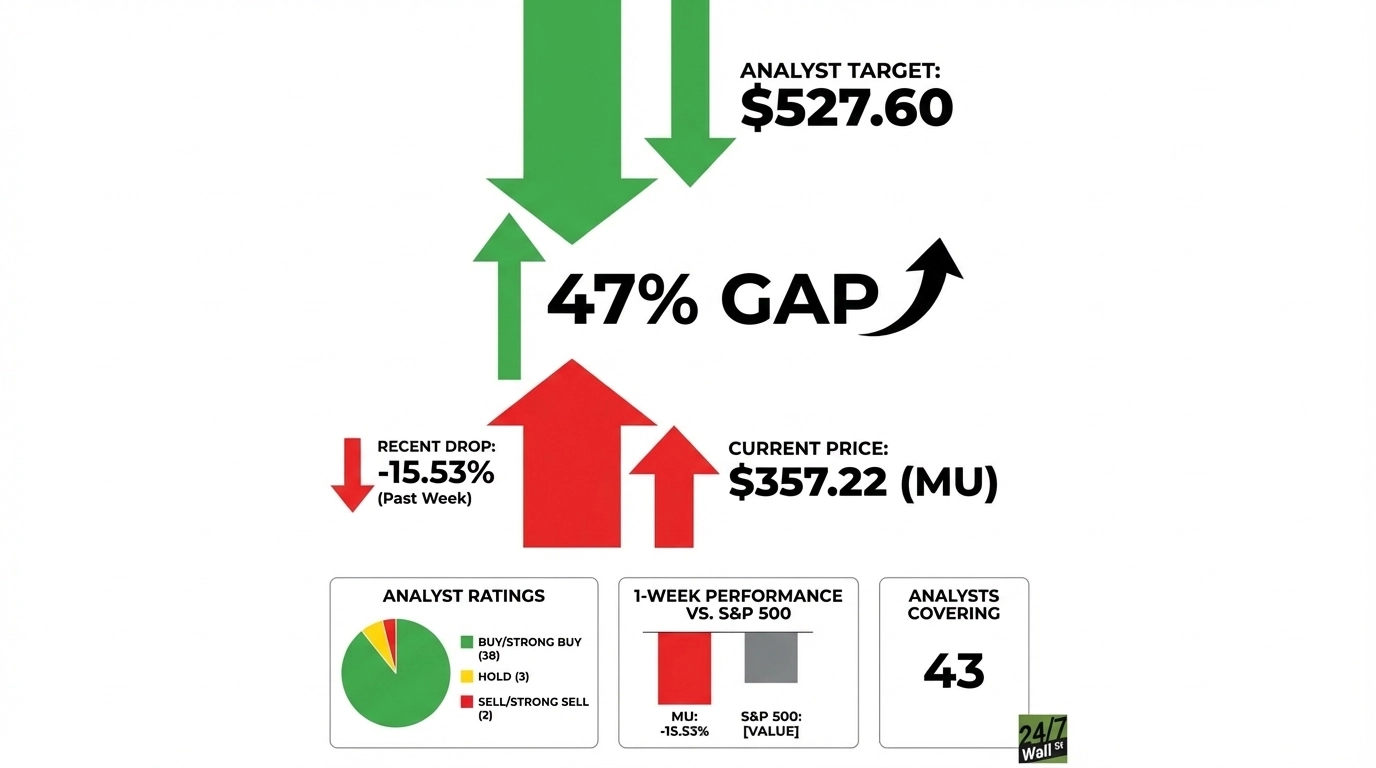

1 month agoWall Street Tells Investors Its Less Excited About Micron Stock

Citi's concern is mainstream DDR5 16GB DRAM prices have fallen 6% since Micron's earnings report, driven by fears that TurboQuant, an algorithm-based memory compression technology, will structurally reduce memory demand. Citi isn't buying it.

Tech industry

from24/7 Wall St.

2 months agoAMAT and Micron still winning in AI trade despite QQQ and sector weakness

The need for higher performance and more energy-efficient chips is driving high growth rates for leading-edge logic, high-bandwidth memory and advanced packaging. These are areas where Applied is the process equipment leader, and we expect to grow our semiconductor equipment business over 20 percent this calendar year.

Artificial intelligence

from24/7 Wall St.

4 months ago3 Top Tech Stocks to Buy if You Want to Outperform Next Year

All three are riding the AI megatrend and have strong revenue visibility beyond 2026. These companies are on the "frontline" when it comes to AI hardware. Data centers are being built out at a record pace, and is not the only company that is benefiting from it. The market is starting to move past NVDA stock and is pouring into other satellite AI beneficiaries who are seeing explosive upward momentum one after the other.

Business

[ Load more ]