"Revenue surpassed $1 billion for the quarter, increasing 46% year over year, supported by the Helly Hansen acquisition and steady brand performance. Adjusted operating income climbed 48% to $150.3M, and adjusted EPS rose 26%. Importantly, margin performance improved rather than deteriorated. Adjusted gross margin expanded to 46.8%, and adjusted operating margin reached 14.8%, up 30 basis points year over year."

"At $64.82, the stock trades at roughly 10x forward earnings based on 2026 guidance, a valuation that appears undemanding if projected earnings growth materializes. With initial 2026 guidance calling for high-single-digit revenue growth and mid-teens EPS expansion, the earnings call will focus on tariff impacts, Helly Hansen integration execution, and sustained margin expansion."

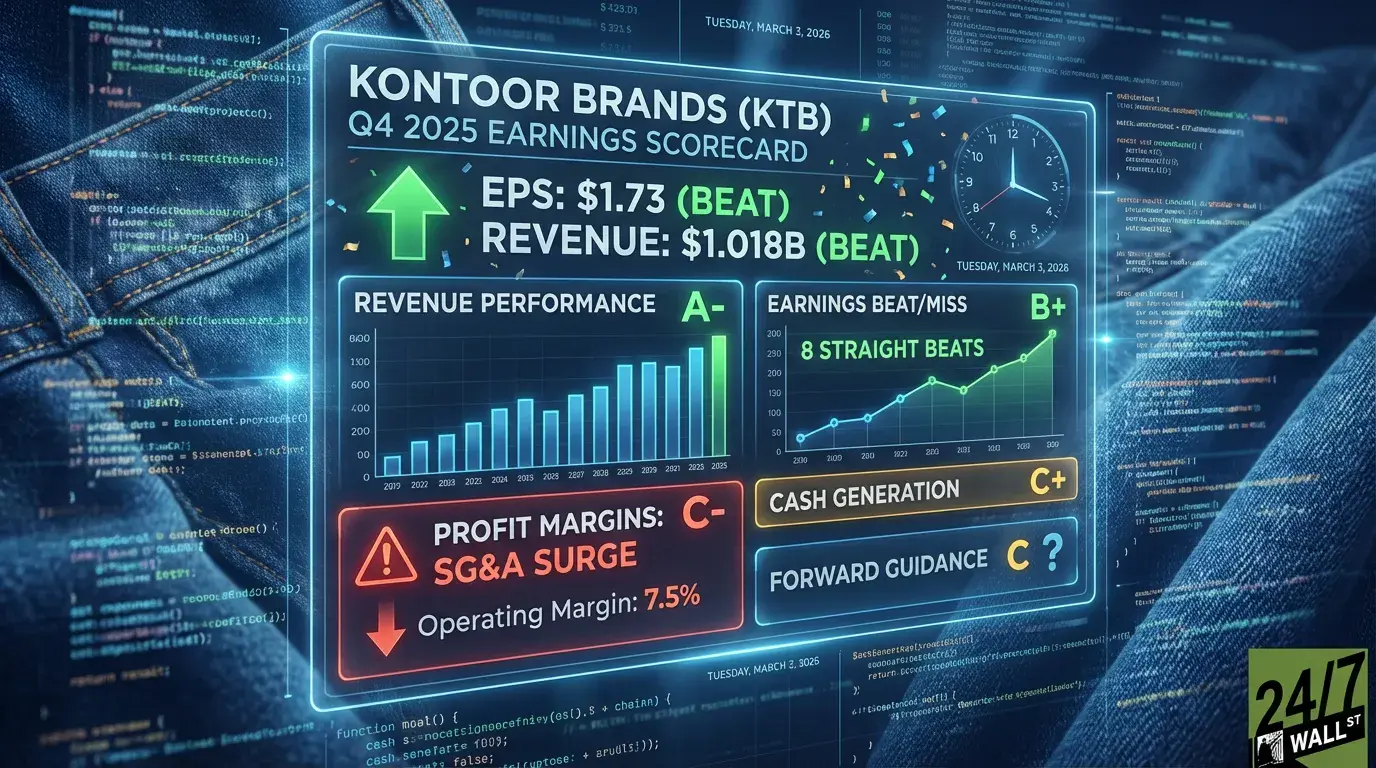

Kontoor Brands delivered a double beat in Q4 2025, reporting adjusted EPS of $1.73 versus $1.67 consensus and revenue of $1.018 billion against a $988.8 million estimate. Revenue increased 46% year over year, driven by the Helly Hansen acquisition and steady brand performance. Adjusted operating income climbed 48% to $150.3 million, while adjusted EPS rose 26%. Margin performance strengthened rather than weakened, with adjusted gross margin expanding to 46.8% and adjusted operating margin reaching 14.8%, up 30 basis points year over year. At $64.82, the stock trades at approximately 10x forward earnings based on 2026 guidance. Initial 2026 guidance projects high-single-digit revenue growth and mid-teens EPS expansion, with focus areas including tariff impacts, Helly Hansen integration execution, and sustained margin expansion.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]