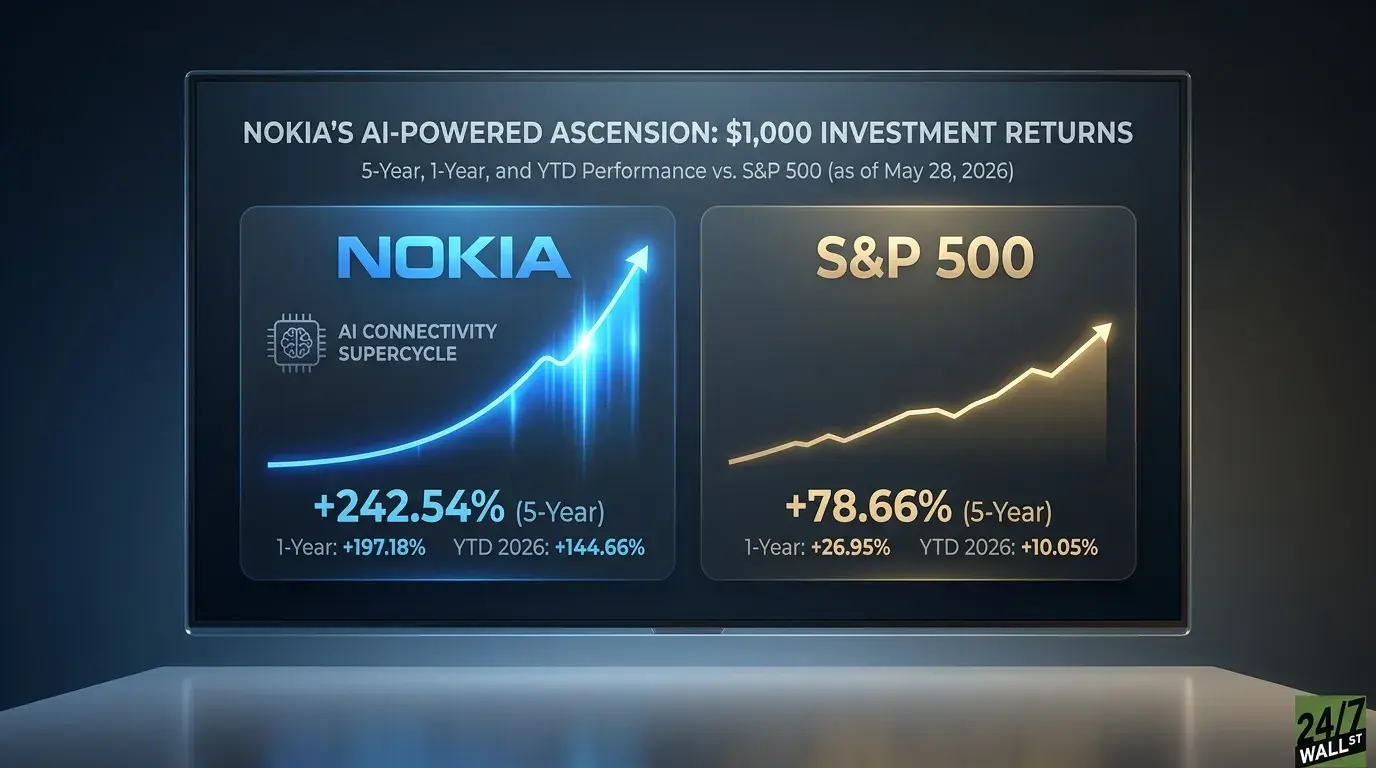

Nokia spent years restructuring and lagged competitors in the 5G market, delivering limited shareholder returns. A pivot began in 2024 with the acquisition of Infinera to expand data center connectivity capabilities, with the deal closing in February 2025. A new CEO repositioned the company around an “AI connectivity supercycle.” In Q4 2025, Nvidia made a $1.0 billion equity investment and formed an AI-RAN partnership, lifting the stock to three-year highs and changing market expectations. Performance gains were concentrated in the past 12 months. The bull case depends on AI-RAN converting into hyperscaler design wins, optical networking growth, and management’s 2028 operating profit targets, supported by a valuation re-rating. The bear case cites a high trailing P/E, a lower consensus target, currency headwinds, and weakening Greater China revenue.

"The pivot started in 2024 with the announcement of the acquisition of Infinera, a U.S. optical networking player that gave Nokia real exposure to data center connectivity. The deal closed in February 2025, and weeks later Justin Hotard, a former Intel data center executive, took over as CEO and repositioned the company around an "AI connectivity supercycle." The real catalyst came in Q4 2025, when Nvidia made a $1.0 billion equity investment alongside an AI-RAN partnership. The stock reached three-year highs, and the narrative shifted."

"Nokia crushed the S&P 500 across every window, but the win is heavily back-loaded. Almost all the five-year gain came in the past 12 months as the AI thesis took hold. Investors who held through years of flat trading were rewarded, while latecomers chasing the 46.3% one-month surge are paying significantly higher prices."

"The bull case for Nokia rests on the AI-RAN partnership with Nvidia converting into hyperscaler design wins, Optical Networks continuing to compound (up 17% in constant currency in Q4 2025), and management hitting its 2028 target of €2.7 billion to €3.2 billion comparable operating profit. Ultimately, the bull case hinges on a re-rating from a telecom multiple to an AI infrastructure multiple."

"The bear case centers on a trailing P/E near 98 and an analyst consensus price target of $12.90, which is well below the current price. Currency headwinds, declining Greater China revenue, and Infinera i"

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]