"Converting a traditional IRA to a Roth IRA sounds straightforward: pay taxes now, enjoy tax-free growth later. But the conversion creates income that ripples through the tax code in unexpected ways. That converted amount increases your adjusted gross income for the year, potentially triggering higher tax brackets, Medicare surcharges, and taxation of Social Security benefits that would otherwise remain untaxed."

"A conversion affects your Medicare premiums two years later due to the lookback period. Medicare premium surcharges kick in at income thresholds that create cliff effects-where a modest conversion can trigger substantial additional annual healthcare costs that persist for a full year. This makes conversion timing critical for anyone within two years of Medicare eligibility, as the lookback period means today's conversion affects premiums years later."

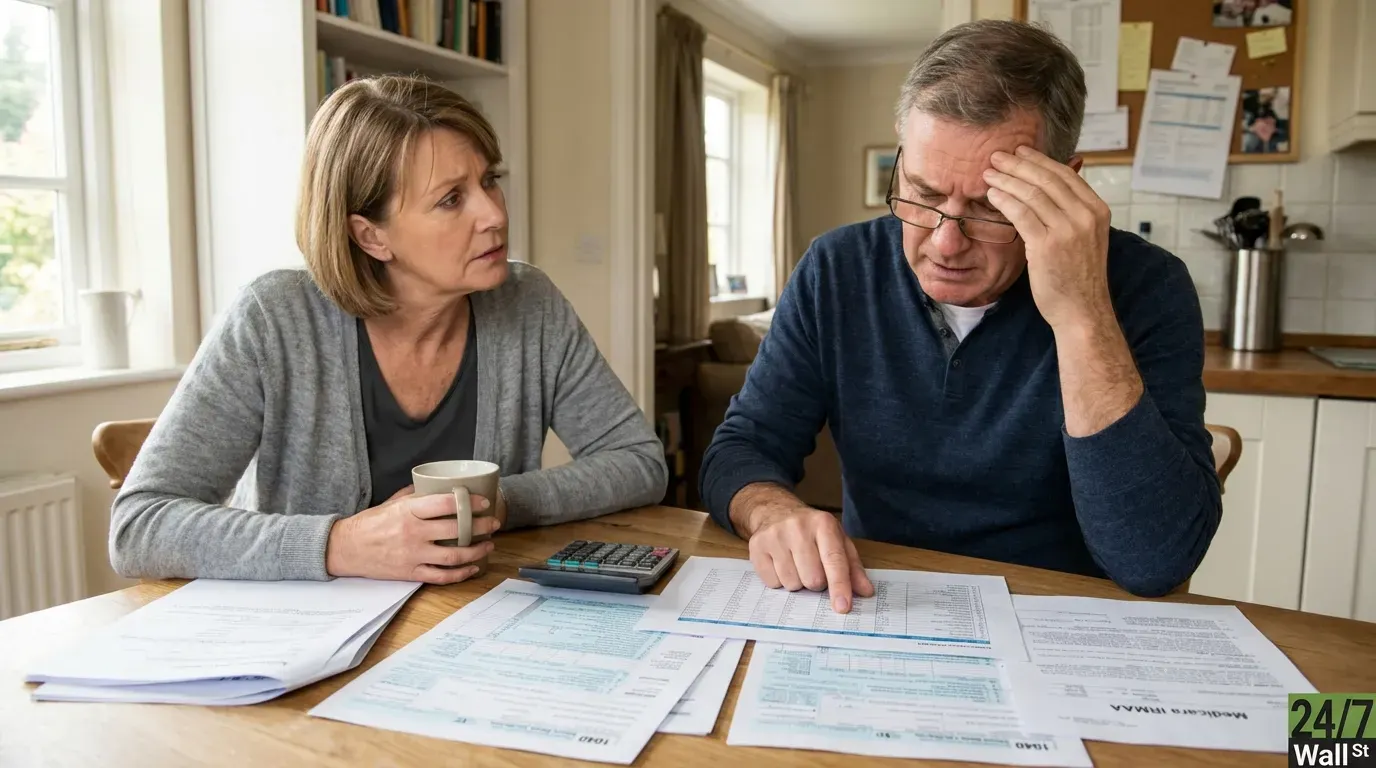

Converting traditional IRA funds to a Roth increases adjusted gross income for the conversion year, which can push taxpayers into higher marginal tax brackets and reduce or eliminate income-based deductions. The conversion amount can raise taxes on other income pushed into higher brackets, creating a compounding cost that diminishes long-term benefits. For Medicare beneficiaries or those nearing eligibility, conversions affect Income-Related Monthly Adjustment Amounts (IRMAA) determined by a two-year lookback, producing cliff effects where modest conversions trigger sizable premium surcharges that persist for a year. Conversion timing and amount therefore require careful tax and benefits planning.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]