"For decades, semiconductor cycles followed a fairly predictable sequence. Demand improved, companies bought more equipment to make more chips, unit shipments increased so that supply exceed demand, and pricing eventually weakened as oversupply returned to the market. Investors therefore learned to focus primarily on unit growth because pricing historically lagged demand rather than led it."

"The current semiconductor recovery is not being driven by a surge in semiconductor units. Instead, it is being driven by constrained supply initially, then by a shortage. In many respects, memory suppliers have inverted the traditional semiconductor cycle by limiting capacity additions as a result of increased Capex (capital expenditure) spend in recent years in anticipation of strong demand for AI and concomitant memory chips."

"This did not happen accidentally. Following the severe downturn that began in 2022, memory manufacturers spent several years cutting capital expenditures, delaying wafer fab equipment purchases, and slowing capacity expansion. Suppliers became far more disciplined after watching prior cycles destroy profitability through overspending."

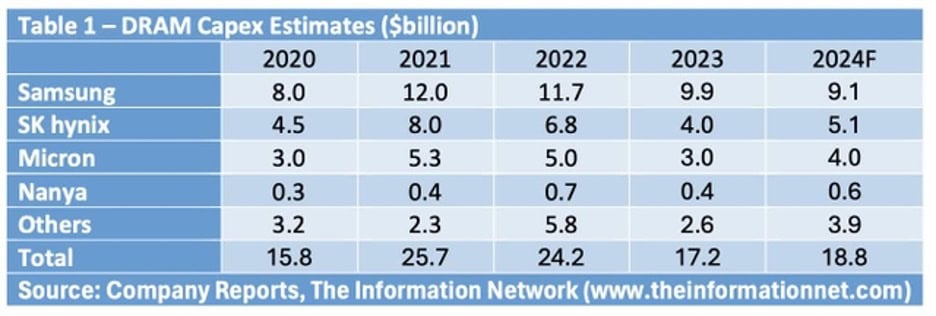

"Memory Pricing Trends: The DRAM industry, including leaders like Micron and Samsung Electronics Co., Ltd. (OTCPK:SSNLF), has observed a strategic pullback in memory production capacity investments (capex), as shown in Chart 1. Micron aims to allocate approximately 30% of its sales to capital expenditures and around 10% of its sales to research and development. These allocations are in line with the practices of industry peers."

Semiconductor cycles historically followed a pattern where demand improved, companies expanded equipment to increase chip output, shipments rose, supply exceeded demand, and pricing weakened. Investors typically tracked unit growth because pricing tended to lag demand. The current recovery differs, especially for memory. It is driven first by constrained supply and then by shortages rather than by a surge in units. Memory suppliers have limited capacity additions after increasing capital expenditure in anticipation of AI-driven demand. After the severe downturn beginning in 2022, memory manufacturers cut capex, delayed wafer fab equipment purchases, and slowed capacity expansion. This discipline followed experience with earlier cycles that destroyed profitability through overspending. Memory pricing and capex trends show strategic pullbacks in production investment, with firms allocating significant portions of sales to capex and smaller portions to R&D.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]