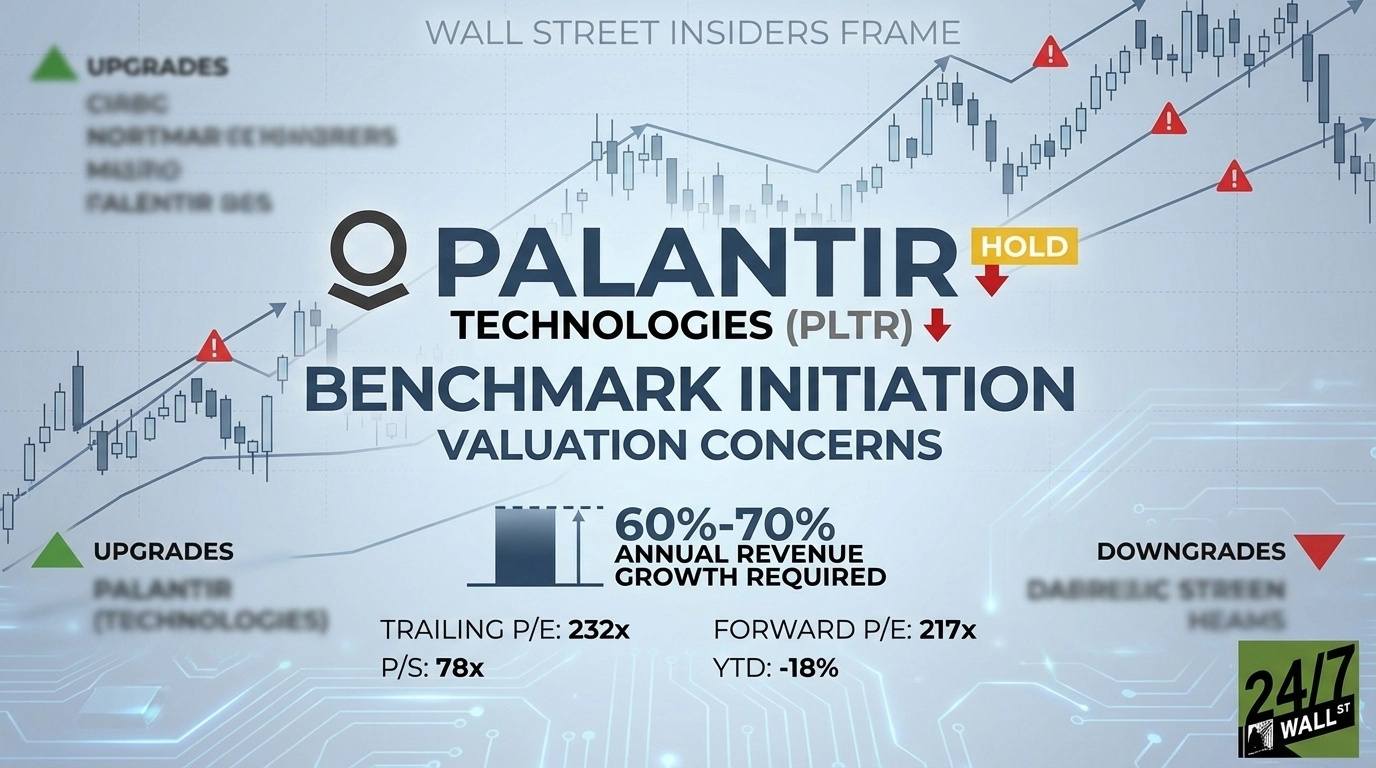

"Benchmark's Yi Fu Lee acknowledges Palantir's AI-powered automation platform, which delivers real-time decision support to government and commercial customers, and recognizes the company's strong fundamentals and leadership under CEO Alex Karp. The problem is valuation."

"Palantir's own guidance for FY 2026 calls for revenue of $7.19 billion at the midpoint, representing 61% year-over-year growth. That figure lands squarely inside the 60% to 70% range Benchmark says is required just to justify current prices."

"The stock trades at a trailing P/E of 232x and a forward P/E of 217x, with a price-to-sales ratio of 78x. These multiples leave almost no margin for error."

Benchmark analyst Yi Fu Lee initiated a Hold rating on Palantir Technologies due to concerns over its high valuation. The stock needs sustained 60% to 70% annual revenue growth to avoid downside risks. Despite strong fundamentals and a robust AI-powered platform, the current price reflects optimistic growth expectations, leaving little room for deceleration. Palantir's guidance for FY 2026 indicates revenue growth of 61%, which barely meets the required threshold. The stock's high P/E ratios and significant year-to-date decline further complicate its investment appeal.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]