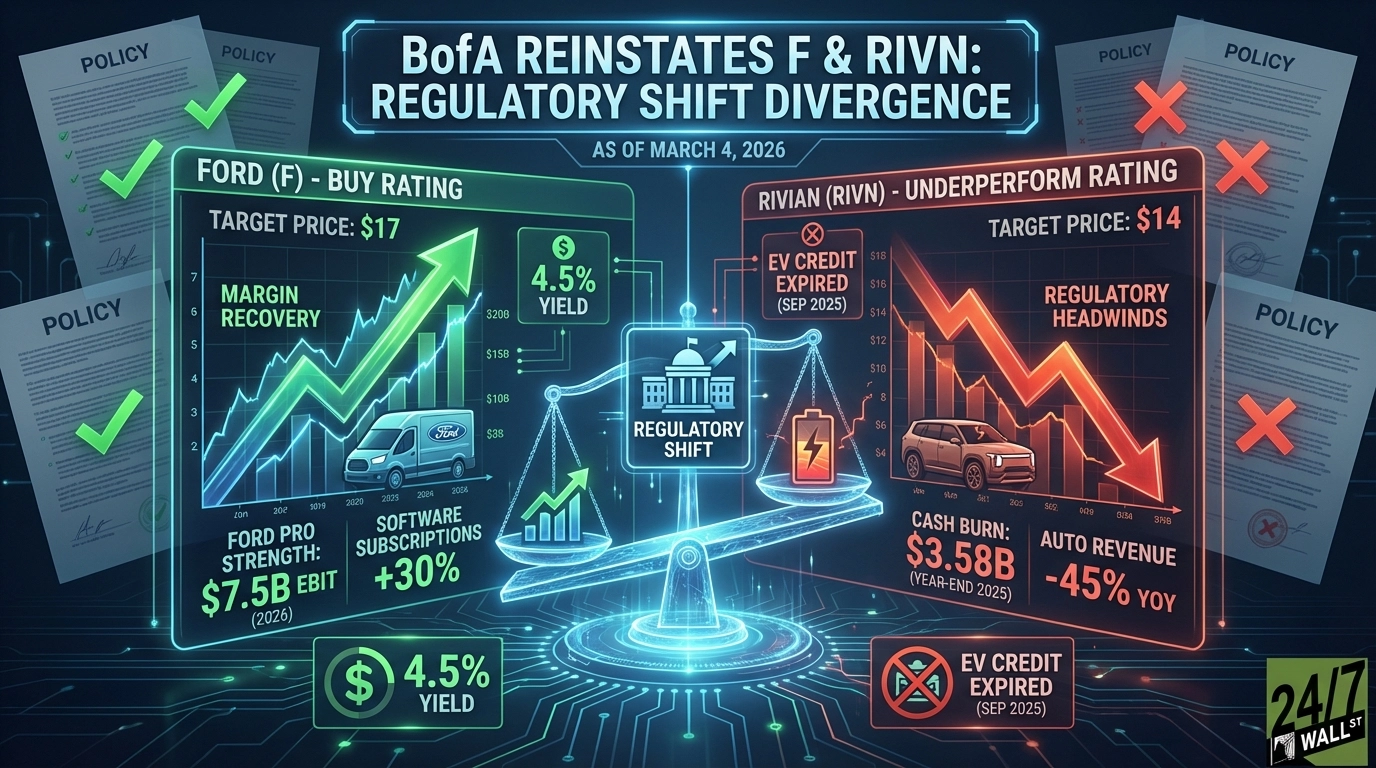

"Ford Pro, the commercial vehicle segment, is guiding for $6.5 billion to $7.5 billion in EBIT for 2026, and paid software subscriptions in that segment grew 30% in 2025. Ford Credit delivered a 55% YoY jump in full-year EBT to $2.6 billion. These are not speculative numbers. BofA expects Ford to progress from a 4.8% EBIT margin in 2026 toward its stated 8% adjusted EBIT margin target by 2029."

"Rivian's Q4 automotive revenue collapsed 45% YoY, driven by a $270 million collapse in regulatory credit sales and softer R1 deliveries after the federal EV tax credit expired on September 30, 2025. BofA's $14 Underperform target is notably below where the stock trades today at $15.105, and it's even more bearish than you'd expect given that the broader analyst consensus carries a $18 target."

Bank of America has taken opposing stances on two major auto stocks, reflecting divergent business models and regulatory exposure. Ford receives a Buy rating with a $17 price target, significantly above the $13.99 consensus, driven by strong fundamentals including Ford Pro's $6.5-7.5 billion EBIT guidance for 2026, 30% growth in paid software subscriptions, and Ford Credit's 55% year-over-year EBT increase to $2.6 billion. The bank expects Ford's EBIT margin to expand from 4.8% in 2026 toward an 8% target by 2029. Conversely, Rivian receives an Underperform rating with a $14 target, below both its current trading price and the $18 consensus target. Rivian's Q4 automotive revenue collapsed 45% year-over-year, driven by a $270 million decline in regulatory credit sales and softer R1 deliveries following the federal EV tax credit expiration.

#ford-vs-rivian #ev-regulatory-credits #auto-industry-earnings #stock-ratings #electric-vehicle-market

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]