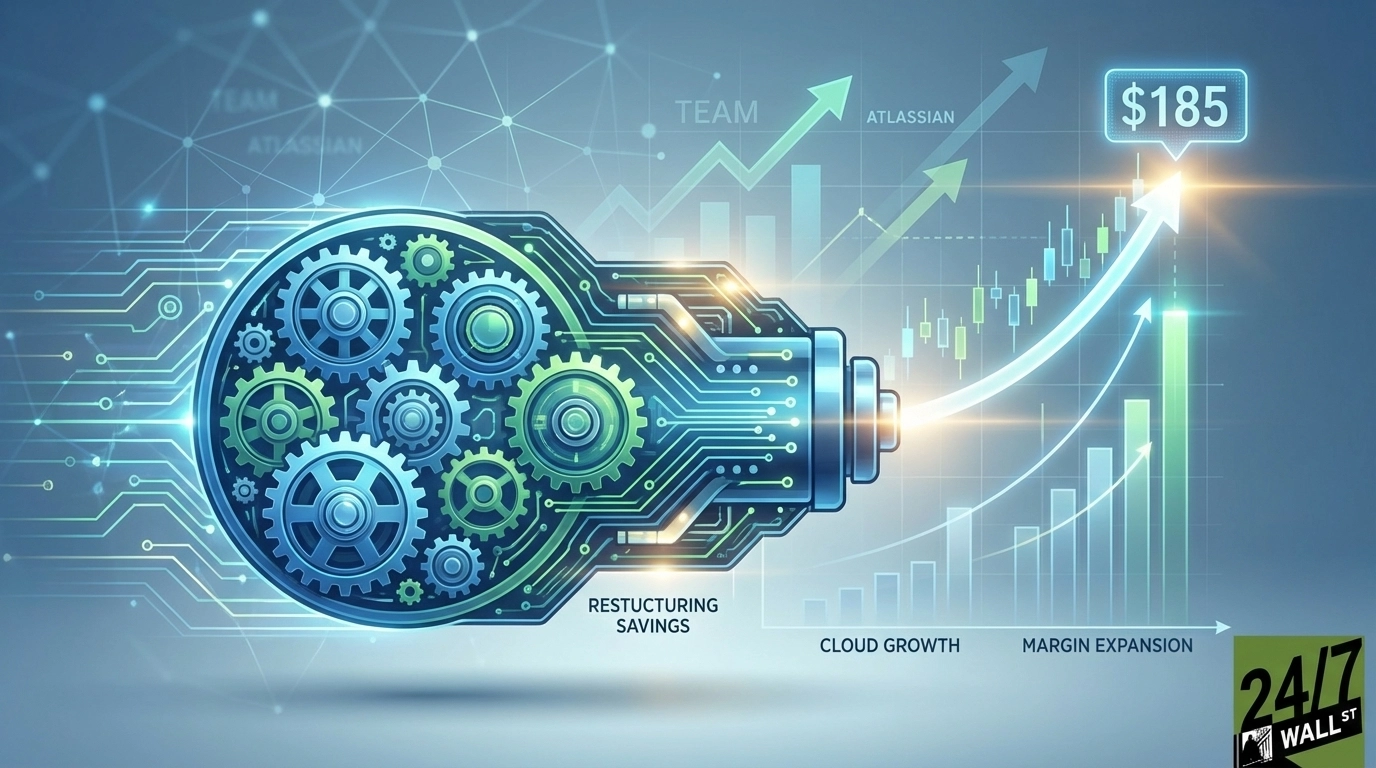

"Mizuho lowered its target from $205 to $185, but the firm is clear that the revision reflects comparable multiple compression across the software sector, not any deterioration in the underlying business thesis. The core of the bull case rests on Atlassian's restructuring, which eliminated 10% of its workforce, or roughly 1,600 employees."

"The $55.7 million in restructuring charges taken in Q1 FY26 are now lapping, and the payoff is visible. Non-GAAP operating margin reached 27% in Q2 FY26, up 1 percentage point year over year, with Q3 guided to ~27.5%. This operating leverage means more of each revenue dollar flowing toward long-term free cash flow growth."

"Atlassian posted its first-ever $1 billion Cloud revenue quarter in Q2 FY26, up 26% year over year, with cloud net revenue retention above 120% for the third consecutive quarter. Remaining performance obligations hit $3.81 billion, up 44% year over year, signaling locked-in future revenue that supports compounding returns."

Atlassian shares have declined 53.47% year-to-date and 150% over the past year from a $242 peak. Mizuho maintains an Outperform rating with a $185 price target, reflecting sector-wide multiple compression rather than business deterioration. The bull case centers on restructuring benefits from eliminating 1,600 employees, which drive margin expansion and accelerate GAAP profitability. Non-GAAP operating margins reached 27% in Q2 FY26 with Q3 guidance at 27.5%. Cloud revenue hit $1 billion in Q2 FY26, growing 26% year-over-year with net revenue retention above 120%. Remaining performance obligations reached $3.81 billion, up 44% year-over-year, indicating locked-in future revenue. GAAP operating margin is guided to approximately 0% in Q3 FY26, approaching breakeven.

#atlassian-stock-valuation #restructuring-and-profitability #cloud-revenue-growth #operating-margin-expansion #software-sector-multiples

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]