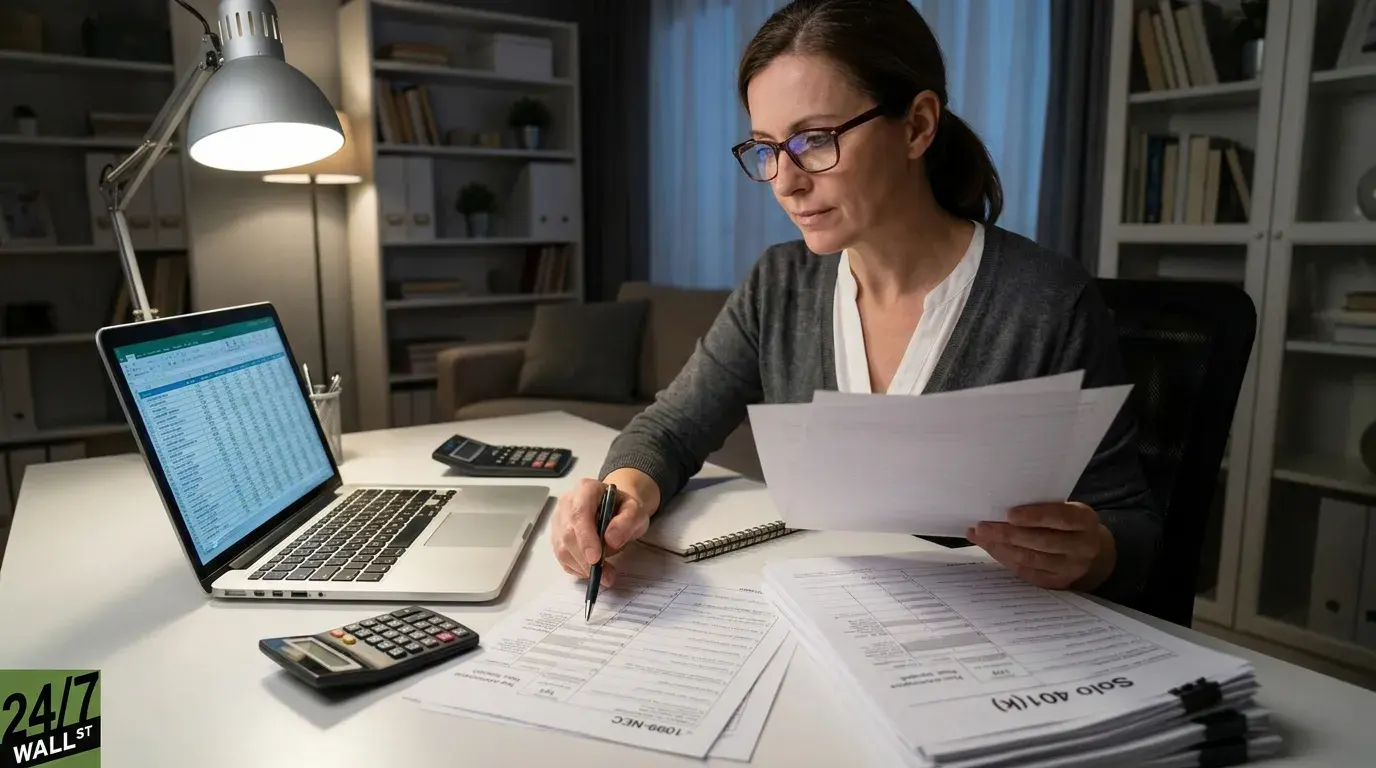

"Sheltering another $40,000 to $50,000 of pre-tax income drops the federal bill by roughly $13,000 to $16,000 a year before any state savings. With core PCE running at 3.2% year-over-year and services inflation at 3.4%, that is real purchasing power preserved at today's inflation ra"

A $24,500 employee deferral cap applies across all 401(k), 403(b), and SAR-SEP plans an individual participates in, so a workplace plan can exhaust that limit. A separate annual addition cap under Internal Revenue Code section 415(c) limits total contributions from an employer, including both employee and employer amounts, to $72,000 in 2026 per unrelated employer. An expert-witness consulting practice treated as an unrelated employer can therefore receive its own $72,000 contribution bucket. For a sole proprietor, the Solo 401(k) employer profit-sharing contribution is calculated as 25% of net self-employment earnings after the 50% SE tax adjustment, producing an effective rate around 20% of net 1099 income. On $200,000 net income, this can yield roughly $40,000 to $50,000 in employer contributions, potentially reducing federal taxes by about $13,000 to $16,000 before state savings.

Read at 24/7 Wall St.

Unable to calculate read time

Collection

[

|

...

]